Breaking down every calculation in our L4/L5 financial planning tool - specifically for tech employees working in India

Disclaimer (Please Read)

This article and spreadsheet are for educational purposes only. They do not constitute personalized financial, tax, legal, or investment advice.

I am not a certified financial planner, tax advisor, chartered accountant, investment advisor, or legal professional. The content is based on general principles, public information, and personal research.

Tax laws, rules, and regulations (including FY 2025–26 assumptions) change frequently. Calculations are simplified and may not reflect your exact situation. Always verify current rules and consult qualified professionals before acting.

All investments involve risk. No outcomes are guaranteed. Examples and assumptions used (income, expenses, family setup, etc.) may not apply to you and must be adjusted to reflect your reality.

This tool assumes resident Indian tax status. If you have foreign income, assets, or complex residency issues, seek specialized advice.

By using this content, you acknowledge that:

You use it at your own risk

You will seek professional guidance before major decisions

No advisory or fiduciary relationship is created

The author assumes no liability for any outcomes

Financial planning is not a one-time ritual—it needs regular review and professional validation.

Download the spreadsheet, make it yours, and share your learnings.

Let's normalize talking about financial preparedness in the AI age.

Because the wave is coming. The only question is whether you'll be ready.

WHEN IN DOUBT, CONSULT A QUALIFIED PROFESSIONAL. Your financial future is too important to leave to a spreadsheet alone.

⚠️ How to Read This Article

This is a 10,000+ word technical breakdown. Here's how to use it:

If you're skimming (5 minutes):

Read only the sections relevant to YOUR situation

Check the assumptions against your reality

Ignore calculations that don't apply to you

If you're implementing (30 minutes):

Read sections matching your CTC/situation

Download the spreadsheet

Replace ALL sample numbers with your actual data

If you're critiquing (full read):

Every number here is based on specific assumptions

All conclusions are conditional ("if X, then Y")

This is a framework, not financial advice

Adjust inputs → outputs change dramatically

Critical reminder: This article explains methodology, not prescribes outcomes. Your mileage WILL vary.

Who This Is For (And Who It's Not)

This article and spreadsheet are specifically designed for:

Tech professionals (L4/L5 level) working and living in India - whether you're in Bangalore, Pune, Hyderabad, Gurgaon, or any other Indian city. You're paying taxes to the Indian government, dealing with EPF/PPF/NPS, navigating Indian tax regimes (Old vs New), supporting family back in your hometown, and worried about AI automation affecting your career in the Indian tech ecosystem.

This is NOT for:

Indian immigrants working in the US (H1B, Green Card holders, US citizens) - that's a different article with completely different tax calculations, retirement accounts (401k, Roth IRA), and immigration considerations

Employees working remotely for foreign companies while in India (tax complexity requires professional advice)

Business owners or entrepreneurs (different financial planning needs)

Freelancers with highly variable income (though principles can be adapted)

If you're an Indian employee working for Indian or multinational companies in India, earning your salary in INR, and planning your future in India - this framework may be useful to you.

Why This Article Exists

Here is a comprehensive financial planning spreadsheet for Indian tech employees (L4/L5 level) preparing for AI disruption. Within hours, people asked:

"Why did you assume ₹40 lakhs CTC?"

"How did you calculate income tax with the new FY 2025-26 rules?"

"What's the logic behind a 12-month emergency fund?"

"Why these specific investments - EPF, PPF, NPS, ELSS?"

Fair questions.

So here's the complete breakdown of every assumption, every formula, and every calculation in that spreadsheet. Not because I want you to accept my numbers blindly - but because I want you to understand the methodology so you can plug in YOUR numbers.

This is built for the Indian context:

Indian Tax Year (FY 2025-26)

Indian retirement accounts (EPF, PPF, NPS)

Indian tax deductions (80C, 80CCD, 80D, HRA exemption)

Indian family obligations (supporting parents in hometown)

Indian living costs (rent in Indian metros, household help, etc.)

Indian financial instruments (ELSS, PPF, FDs, LIC)

Think of this as the "show your work" section of a math exam. Except the stakes are your financial survival in the AI era while navigating the Indian financial system.

The Foundation: Understanding CTC vs Take-Home

Assumption 1: ₹40 Lakh CTC for L4/L5 Employee

Why ₹40 lakhs?

Based on 2024-2025 market data for mid-level engineers (L4/L5) in Indian tech hubs:

L4 (Senior Engineer): ₹25-35 lakhs CTC

L5 (Staff Engineer/Lead): ₹35-50 lakhs CTC

Sweet spot: ₹40 lakhs = upper L4 or lower L5

Your reality might differ:

Bangalore/Pune/Hyderabad pay more than Tier-2 cities

FAANG/unicorn startups pay more than service companies

Domain matters: ML/AI engineers earn 20-30% more

How to adjust: In Sheet 1, Cell B5, change ₹4000000 to YOUR actual CTC. Everything else recalculates automatically.

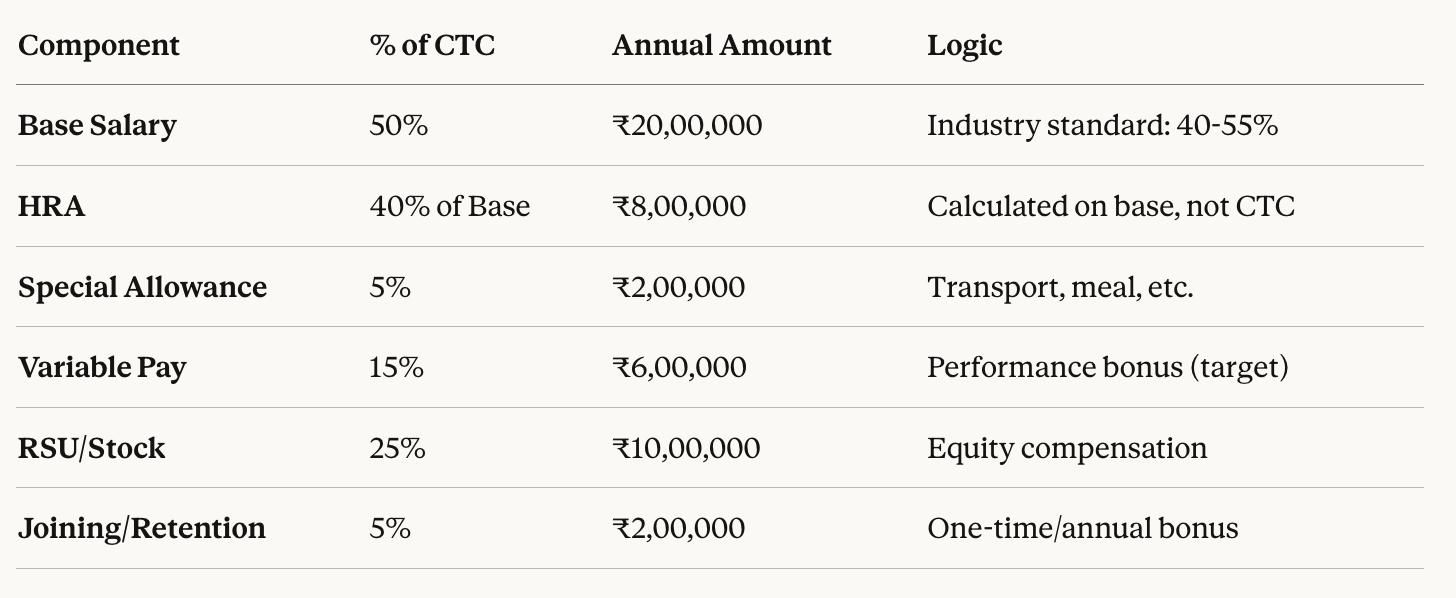

CTC Component Breakdown: The 50-15-25-10 Rule

Here's how I split ₹40 lakh CTC:

Why this split?

50% Base is conservative. Some companies do 60% base, others 40%. Why 50%?

Allows higher employer EPF contribution (capped at 12% of ₹15K/month = ₹21,600/year max)

Balances fixed vs variable compensation

Industry average for tech companies

15% Variable assumes you'll actually get it. Reality check:

Most companies set "target" variable at 15-20%

Actual payout: 0-150% of target based on performance

I assumed 80% payout = ₹4.8L instead of ₹6L

Conservative but realistic

25% RSU is standard for product companies. But here's the catch:

Vests over 4 years typically (25% per year)

Taxed as income when it vests

I calculated only 25% vesting annually = ₹2.5L/year in taxable income

If your RSUs vest monthly, spread it evenly

Your company might differ:

Service companies: Higher base (60-70%), lower/no RSU

Startups: Lower base (40%), higher equity (30-40%)

FAANG: Higher RSU (30-35%)

Adjust the percentages in Sheet 1 to match your offer letter.The Tax Maze: FY 2025-26 New Rules

The Tax Maze: FY 2025-26 New Rules

Why Tax Calculation Gets Complicated

Gross Income ≠ Taxable Income

From ₹40L CTC, here's what actually becomes taxable:

Wait, where did ₹70,000 go?

Variable: Only 80% paid out (₹4.8L instead of ₹6L)

RSU: Only 25% vests this year (₹2.5L instead of ₹10L)

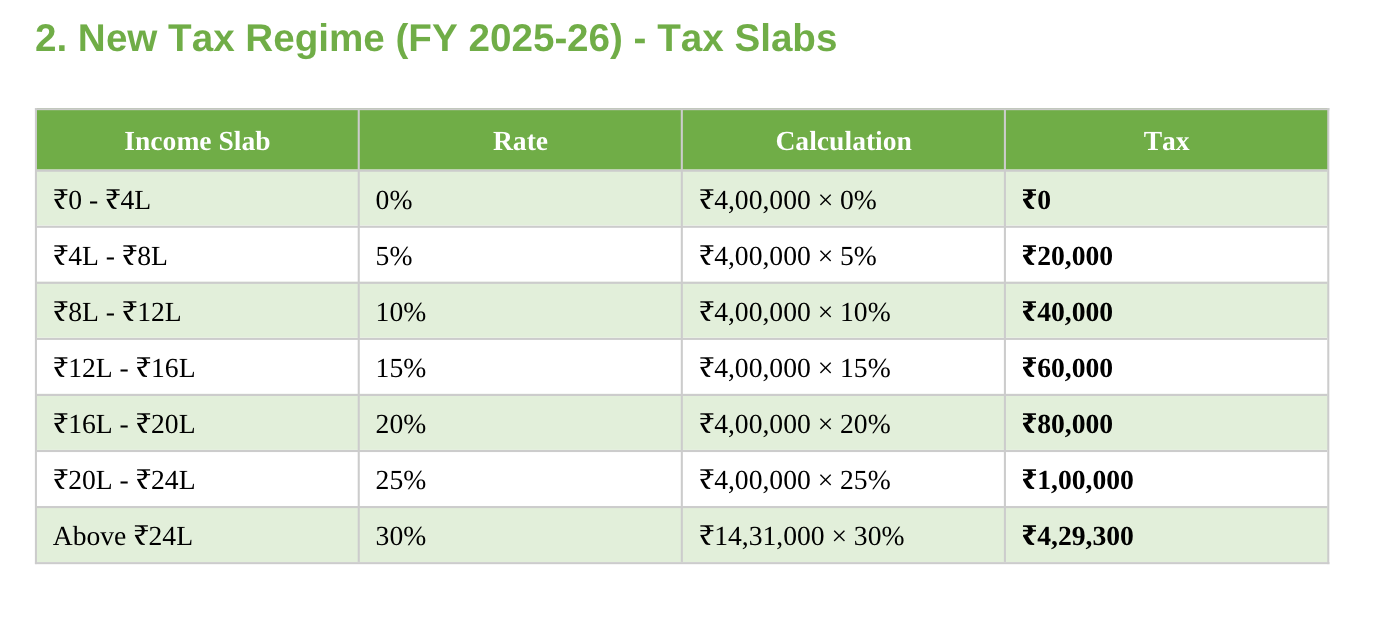

New Tax Regime (FY 2025-26): The Default Choice

Step 1: Calculate Taxable Income

Why ₹75,000 standard deduction?

Increased from ₹50,000 in FY 2024-25

Automatic - no proof needed

Available to EVERYONE in new regime

Why EPF capped at ₹21,600?

Employee contributes 12% of Basic

But only on ₹15,000/month max (₹1,800/month × 12 = ₹21,600/year)

Even if your basic is ₹1.67L/month, EPF contribution maxes out

Step 2: Apply Tax Slabs (New Regime FY 2025-26)

Effective Tax Rate: ~19-20% (₹7.58L on ₹39.3L gross income)

Old Tax Regime: When It Makes Sense

Only if you have LOTS of deductions:

HRA Exemption Calculation (Most confusing part):

HRA exemption = LEAST of three values:

a) Actual HRA received: ₹8,00,000

b) 50% of Basic (if metro) or 40%:

Basic = ₹20L

Metro (Bangalore/Mumbai/Delhi/Kolkata) = 50% = ₹10L

Non-metro = 40% = ₹8L

We assumed metro → ₹10L

c) Rent paid - 10% of Basic:

Assumed rent: ₹30,000/month = ₹3,60,000/year

10% of basic: ₹2,00,000

= ₹3,60,000 - ₹2,00,000 = ₹1,60,000

HRA Exemption = MIN(₹8L, ₹10L, ₹1.6L) = ₹1,60,000

Why so low? Because rent paid is only ₹3.6L but basic is ₹20L. The "rent - 10% basic" formula limits the exemption.

If you pay ₹50,000/month rent:

Rent = ₹6,00,000

Rent - 10% basic = ₹6L - ₹2L = ₹4L

HRA exemption jumps to ₹4L

This is why higher rent increases HRA exemption value.

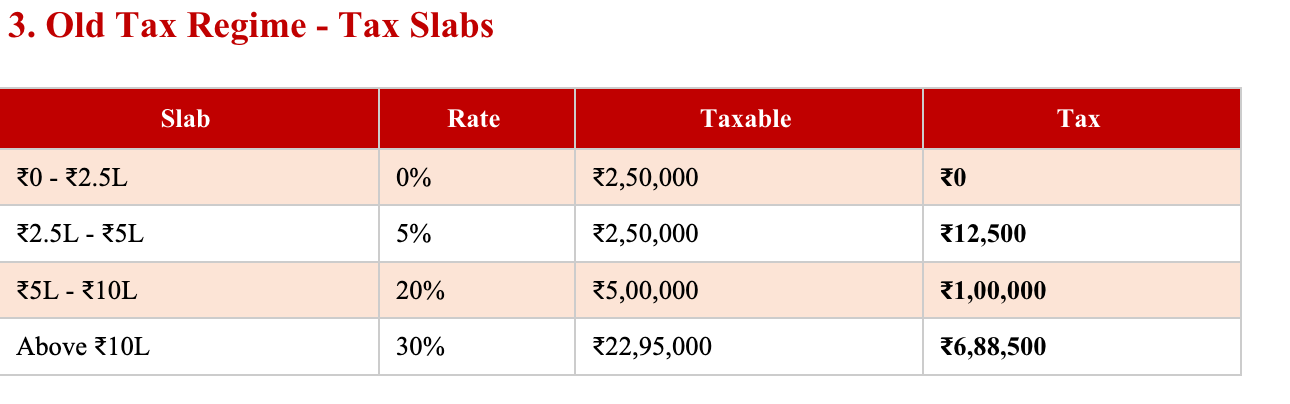

Old Regime Tax Calculation:

Comparison:

New Regime: ₹7,58,470

Old Regime: ₹8,33,040

New Regime saves ₹74,570

When Old Regime wins:

Home loan interest > ₹3L

Parents' health insurance (senior citizen - ₹50K deduction)

Very high 80C investments already locked in

For most L4/L5 employees renting: New Regime is better.

Monthly Take-Home: The Real Number

Sanity check for this example:

Started with ₹40L CTC

Taking home ₹30.5L

Lost ~24% to tax and deductions

From ₹40L CTC in this model:

~77% becomes take-home

~19% goes to income tax

~1% statutory deductions

Remaining ~3% was variable/RSU not paid/vested

Expenses: The 50/30/20 Framework (Indian Edition)

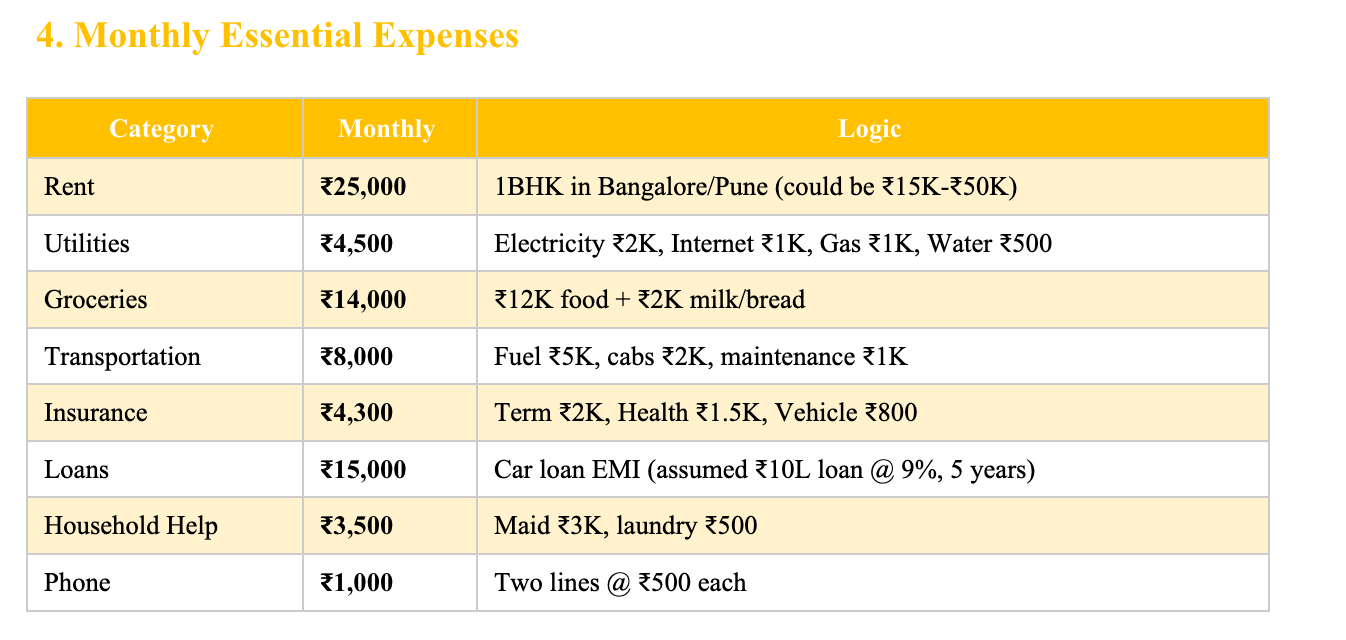

Essential Expenses: ₹80,000-₹1,00,000/month

I assumed single employee, renting, no kids:

If you have kids, add:

School fees: ₹10K-₹50K/month

Daycare: ₹15K-₹30K/month

This could push essentials to ₹1.2L-₹1.5L

If you own a home:

Remove rent (₹25K)

Add home loan EMI (₹40K-₹80K typical for ₹50L-₹1Cr loan)

Net: Essentials increase by ₹15K-₹55K

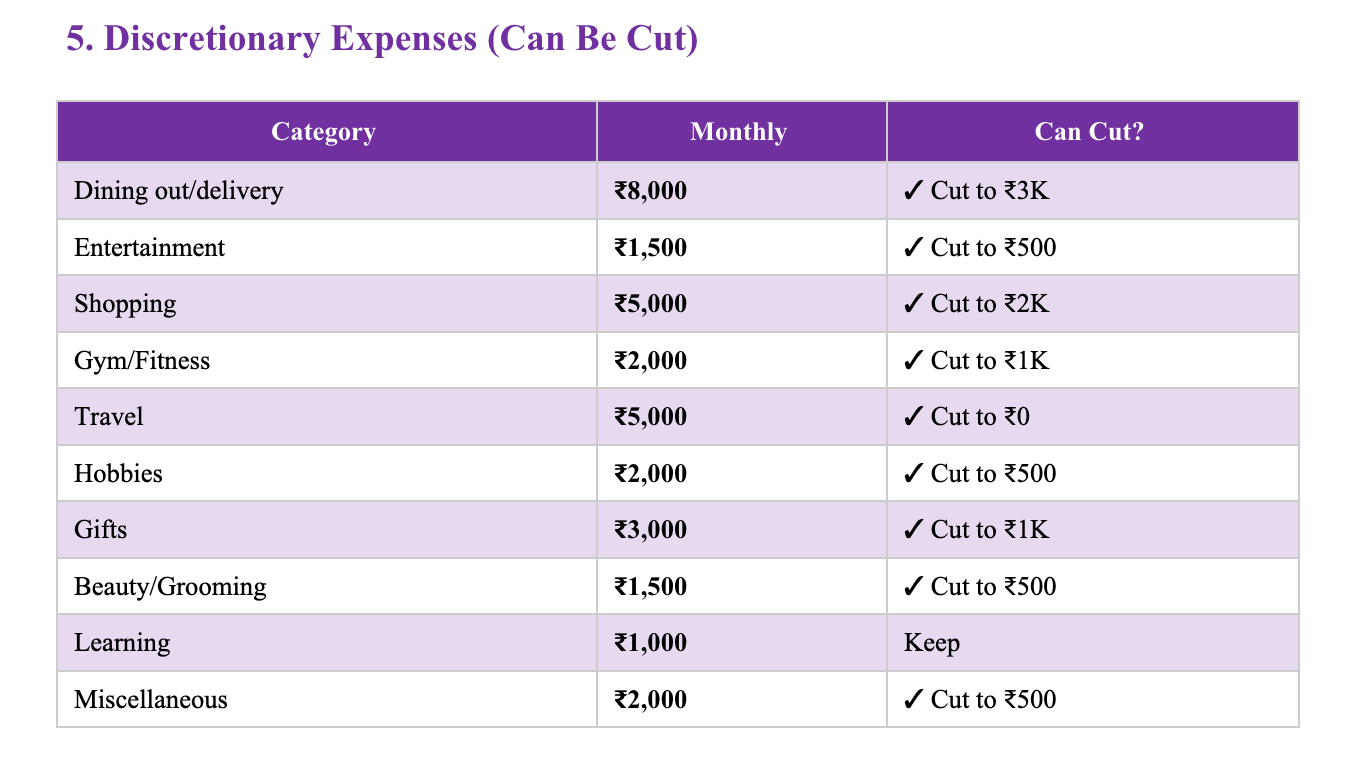

Discretionary Expenses: ₹31,000/month

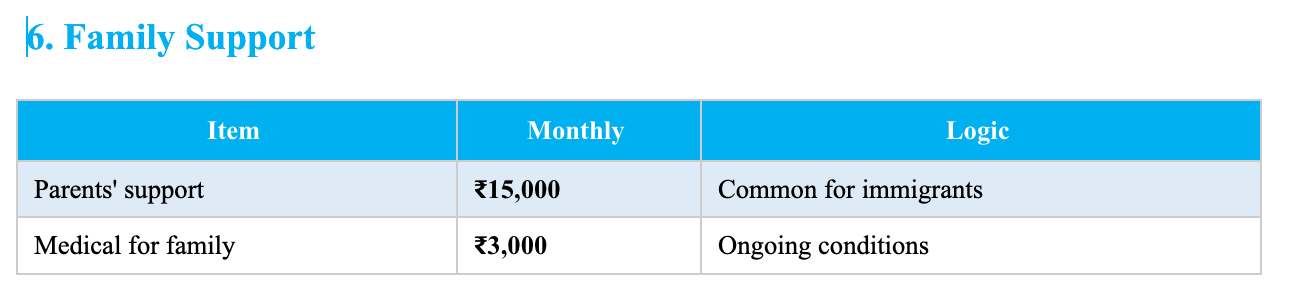

Family Support: ₹18,000/month

Reality for many immigrants:

Sending ₹10K-₹30K/month to parents

Medical emergencies: ₹50K-₹2L unpredictable hits

Siblings' education: Additional ₹10K-₹20K

Total Monthly Expenses:

Essential: ₹75,300

Discretionary: ₹31,000

Family: ₹18,000

Total: ₹1,24,300/month

Monthly surplus: ₹2,53,961 - ₹1,24,300 = ₹1,29,661

Savings rate: 51% (Very high - most people are 20-30%)

Emergency Fund: The 12-Month Rule

Why 12 Months, Not 6?

Traditional advice: 6 months of expenses

AI disruption reality:

Job search for 40+ candidates: 6-9 months average

Career pivot/retraining: 6-12 months

Age discrimination: Adds 3-6 months to job search

Industry switching: 12+ months often needed

The math:

Assume current emergency fund: ₹3,00,000

Covers: 3.6 months

Gap to 12 months: ₹6,93,960

Monthly contribution needed: ₹57,830 (to reach in 12 months)

This is Priority #1 until you hit ₹10L emergency fund.

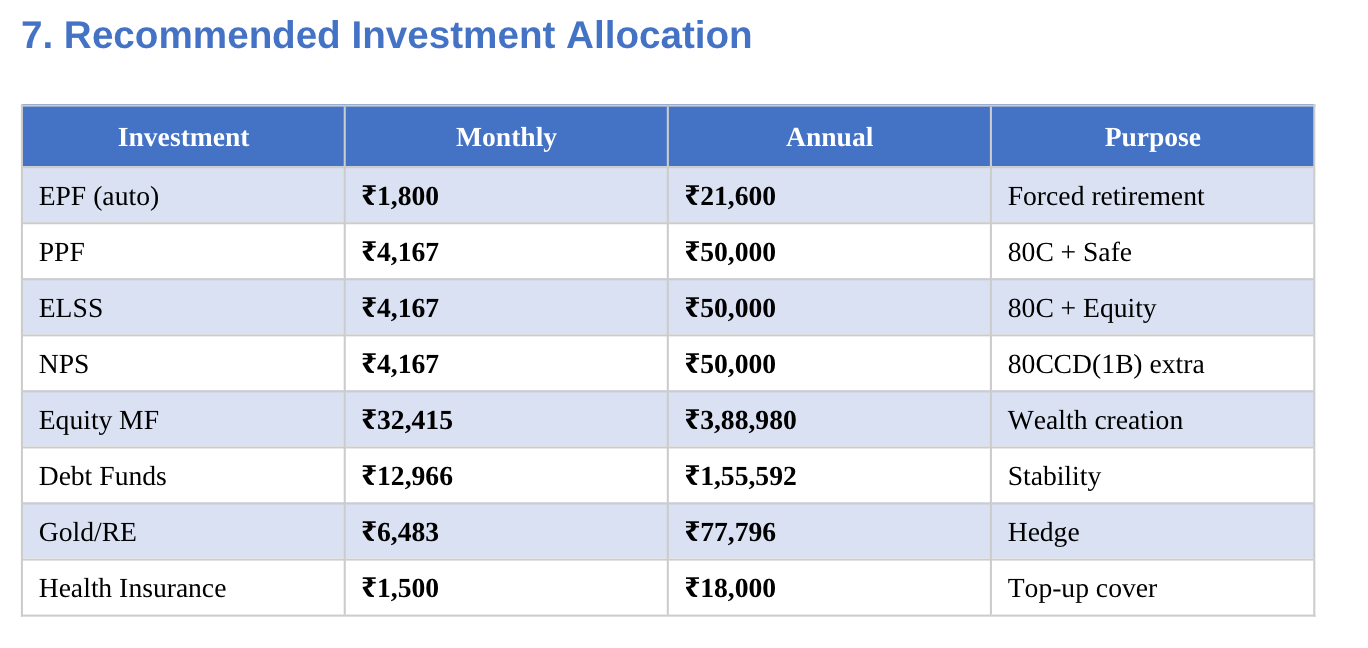

Investment Allocation: The AI-Era Portfolio

After Emergency Fund Is Built

Monthly investable surplus: ₹1,29,661

Why These Percentages?

80C maxed at ₹1.5L:

EPF: ₹21,600 (automatic)

PPF: ₹50,000 (safe, tax-free returns ~7%)

ELSS: ₹50,000 (equity exposure + tax benefit)

Remaining ₹28,400: Life insurance premium or PPF

NPS ₹50K:

Additional deduction under 80CCD(1B)

Saves ₹15,600 in taxes (if 31.2% bracket)

Lock-in until 60, but worth it for tax saving

Equity 25% of surplus:

High growth potential (12-15% historically)

Long-term wealth creation

Ride out volatility

Debt 10% of surplus:

Stability when equity crashes

Liquid for emergencies beyond emergency fund

6-8% returns

Gold/RE 5%:

Hedge against inflation

Diversification

Can be digital gold (more liquid)

Net Worth: The Tracking Metric

What to Include

Assets in this example:

Liquid (₹7,50,000):

Savings account: ₹1,00,000

Emergency fund: ₹3,00,000

FDs: ₹2,00,000

Liquid MF: ₹1,50,000

Investments (₹20,00,000):

EPF: ₹5,00,000 (accumulated)

PPF: ₹3,00,000

NPS: ₹2,00,000

Equity MF: ₹4,00,000

ELSS: ₹1,50,000

Stocks: ₹2,00,000

Debt MF: ₹1,00,000

Gold: ₹1,50,000

Physical (₹10,00,000):

Vehicle: ₹8,00,000

Gold jewelry: ₹2,00,000

Total Assets: ₹37,50,000

Liabilities:

Car loan: ₹6,00,000

Net Worth: ₹31,50,000

Is This Good?

Rule of thumb: Net worth should be (Age / 10) × Annual Income

Example:

Age: 35

Income: ₹30.5L take-home

Target: 3.5 × ₹30.5L = ₹1.07 Cr

Current: ₹31.5L Progress: 29% of target

This is actually pretty good for someone in their early-mid 30s.

By age 40:

Target: 4.0 × ₹30.5L = ₹1.22 Cr

Projected (with ₹70K/month investment @ 12% return): ₹95L

Still need to increase savings/returns

AI Disruption Scenarios: The Stress Tests

Scenario 1: Complete Job Loss

Assumptions:

Zero income immediately

Severance: 3 months (optimistic case)

New job search: 6-9 months (typical range)

Survival math in this model:

With aggressive expense cuts (70% discretionary reduction):

Under these assumptions, this profile could potentially survive 12-17 months depending on expense discipline.

This scenario depends on:

Finding employment within 12 months

Actually cutting discretionary spending

No major medical emergencies

Ability to pause family support temporarily

Scenario 2: 30% Salary Cut

New income: ₹2,53,961 × 0.70 = ₹1,77,772/month

Current expenses: ₹1,24,300/month

Analysis: ₹1,77,772 - ₹1,24,300 = ₹53,472 surplus remains

In this scenario, because the baseline savings rate was ~51%, even with a 30% income reduction, essential expenses are still covered with room for some savings.

However:

Cutting all discretionary (₹31K) provides additional buffer

Reducing family support by 30% (save ₹5.4K) if necessary

Total potential adjustment capacity: ₹36.4K

Under this model, a 30% salary reduction appears manageable with lifestyle adjustments.

Scenario 3: Freelance Transition

Target: 60% of salary = ₹1,52,377/month

Reality spectrum:

Optimistic: 80% of target = ₹1,21,901

Realistic: 60% = ₹91,426

Pessimistic: 40% = ₹60,951

Can this profile survive?

Essential expenses: ₹75,300

Optimistic: ✓ Surplus ₹46.6K

Realistic: ✓ Surplus ₹16.1K

Pessimistic: ❌ Shortfall ₹14.3K

Buffer needed: 3 months of zero income = ₹82,830 × 3 = ₹2,48,490

Current emergency fund: ₹3,00,000 ✓ Meets 3-month threshold

But: Freelancing often has dry periods. A 6-month buffer minimum = ₹4.97L would be more prudent.

Gap: ₹1.97L

The Risk Score: A Subjective Self-Assessment Framework

⚠️ Important Disclaimer About This Section

This "risk score" is a subjective self-assessment index, NOT a scientific measurement.

Unlike a credit score backed by empirical default data, this framework uses:

Subjectively chosen factors

Arbitrary weights (based on judgment, not data)

Self-reported scoring (vulnerable to bias)

It's a heuristic tool for structured thinking, not an analytical prediction.

Think of it like a fitness self-assessment - useful for identifying areas to work on, but not a medical diagnosis.

Use it to:

Identify weak spots in your preparation

Track improvement over time

Structure conversations about readiness

Don't use it to:

Make yes/no career decisions

Compare yourself to others

Predict actual outcomes

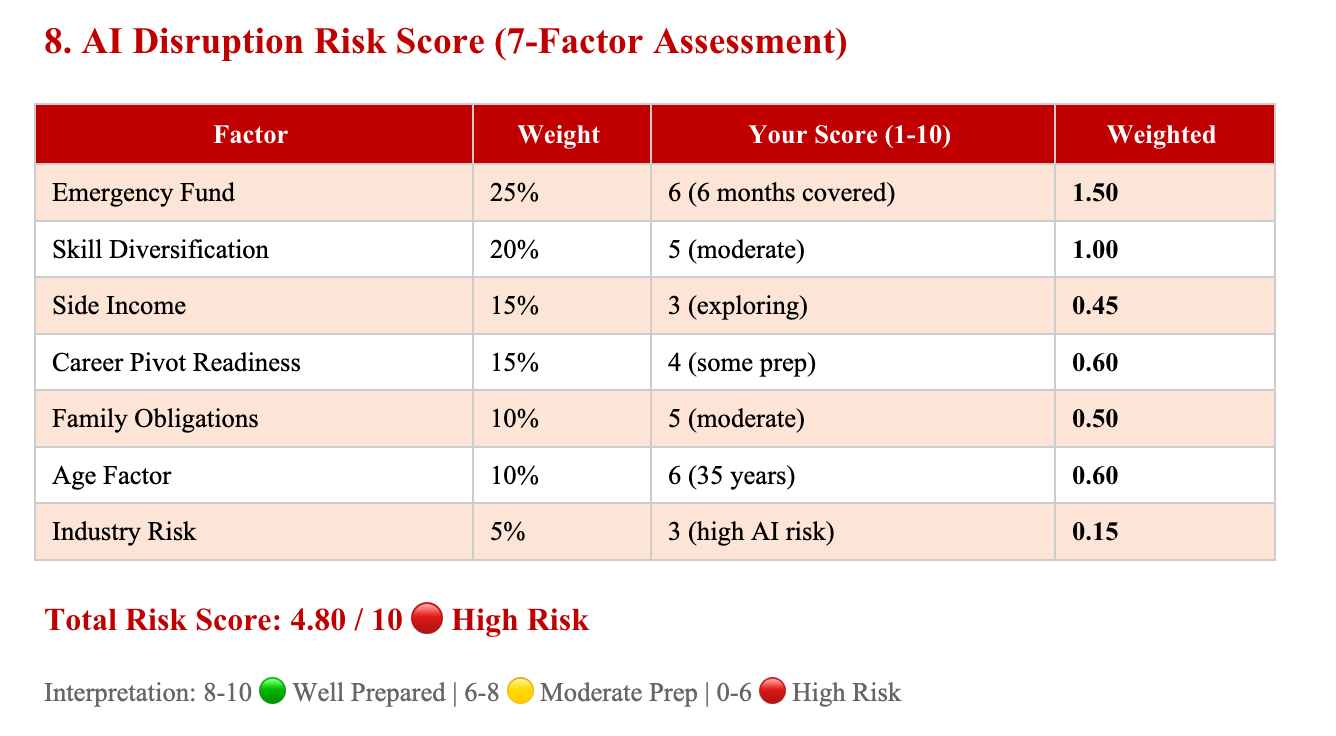

The Risk Score: Measuring Preparedness

Why?

Emergency fund only 6 months (need 12)

Limited skill diversification

No established side income

Not fully ready for career pivot

How to Improve Your Score

From 4.8 → 7.5 in 12 months:

1. Emergency Fund (6 → 10):

Save ₹6L more (₹50K/month)

Weight: 25%

Impact: +1.0

2. Skill Diversification (5 → 8):

Learn 2 adjacent skills (product management, system design)

Weight: 20%

Impact: +0.6

3. Side Income (3 → 7):

Start consulting (₹20K-₹50K/month)

Weight: 15%

Impact: +0.6

New Score: 4.8 + 1.0 + 0.6 + 0.6 = 7.0 → 🟡 Moderate Prep

The Formulas That Matter

Key Excel Formulas Used

1. HRA Exemption:

excel

2. New Regime Tax:

excel

3. Emergency Fund Months:

excel

4. SIP Required for Goal:

excel

5. Runway Calculation:

excel

What I Deliberately Left Out

Things NOT in the spreadsheet:

Crypto - Too volatile for systematic planning

Real estate as primary investment - Most L4/L5 profiles can't afford yet

International investing - LRS limits and complexity

Options trading - Not suitable for core financial planning

Business income - Too variable to model reliably

Inheritance - Cannot plan for unknowns

Why?

Because this tool is designed for methodical financial planning for salaried employees preparing for potential disruption.

Not speculative strategies. Not get-rich-quick approaches. Systematic, calculable, adjustable planning.

Common Questions & Adjustments

"My CTC is ₹25 lakhs, not ₹40 lakhs"

In Sheet 1, change B5 to 2500000

Everything recalculates proportionally:

Tax drops to ~₹3.2L (new regime)

Take-home: ~₹1.65L/month

Emergency fund target: ₹5-6L (instead of ₹10L)

Investable surplus reduces proportionally

The methodology remains the same, outputs scale to your input.

"I have kids and a home loan"

Adjust:

Essential expenses: Add ₹30K-₹80K (kids + EMI)

Discretionary: May need to reduce by ₹10K

Old regime might become more favorable (home loan interest deduction)

In Sheet 2:

Update Section 24(b) with actual home loan interest

Recheck which regime is better for YOUR numbers

"I'm 45, not 35"

Risk factors change:

Job search typically takes 30-50% longer for 45+ candidates

Career pivot becomes more challenging

May need 15-18 month emergency fund (not 12)

Adjust:

Increase emergency fund target

Increase insurance coverage

More conservative investment allocation (40% debt vs 20%)

"I'm in Tier-2 city, expenses are lower"

Adjust downward:

Reduce rent by 40-50% (₹12K-₹15K vs ₹25K)

Reduce transportation by 30%

Essentials drop to ₹55K-₹60K

This proportionally increases your runway and savings capacity.

The Uncomfortable Reality

This spreadsheet may reveal things you'd prefer not to see:

Discretionary spending is higher than you thought

Emergency fund is insufficient

Retirement savings are behind target

That car EMI is stretching your budget

Family obligations may be unsustainable

You may be closer to financial stress than comfortable

That's the point.

Better to see reality clearly now than discover it during a crisis.

What Success Might Look Like

6 months from now, after using this framework:

Emergency fund: ₹6L+ (from ₹3L)

Investment rate: 40%+ of income

Discretionary spending: Cut by 30%

Side income: ₹15K-₹30K/month developing

Insurance: Adequate coverage in place

Tax optimization: Using optimal regime

Skill development: 1-2 new marketable skills in progress

Risk score: 7/10 (from 4.8/10)

You might still face job disruption from AI.

But you'll have 12+ months of runway to navigate it instead of 2 months of panic.

Final Thoughts

This isn't a perfect tool. Your life has nuances no spreadsheet can capture:

Aging parents' health deteriorates

Siblings need emergency support

You want to switch careers

Mental health requires a break

Divorce, medical crisis, accidents

But it's a starting point.

A framework to think systematically about financial resilience. Math you can adjust to YOUR reality.

The assumptions I made are educated estimates based on market data and experience.

Your job is to replace my assumptions with your reality.

Then, quarterly, update it. Track your progress. Adjust your targets.

Because when AI comes for jobs in your sector - and it might - you'll want to answer one question with confidence:

"How long can I navigate this transition?"

And right now, do you know the answer?